Life Insurance for Physicians

For physicians, dealing with the end of life is part of the job. And with each passing year, it’s also an ever-present fact of our own lives. Each step along life’s journey can remind us: life isn’t forever.

We take out school loans. We start a career. We commit to a partner. We create a business. We create a home. We have kids. We anticipate retirement. All these events — life’s best things — are worthy of celebration, yet they also make us think: What will happen to the people we love and the obligations we have when we’re no longer around?

One of the many ways to protect what’s most precious in life after you’re gone is life insurance. The appropriate life insurance policy ensures everyone and everything in your life are OK, even when you’re no longer here.

Like disability insurance, life insurance exists to protect against unforeseen circumstances. A good life insurance plan will take into account factors specific to your unique profile: your age, gender, family medical history, personal medical history, financial obligations, current life situation, and, if you choose, your plans for the future.

That being said, choosing a policy that’s exactly right for you can be daunting on your own. That’s where PearsonRavitz comes in. We know that finding the right policy doesn’t need to be confusing. It just needs to be designed with you in mind.

Scott Ravitz | President of PearsonRavitz + Insurance Expert

The Basics of Life Insurance

Simply put, life insurance offers financial protection for those who depend on you. In the event of your death, your life insurance policy will pay a lump sum of money to your beneficiaries to ensure your family’s financial security.

When you die, your life insurance can be used to cover financial expenses and pay off debt, enable your family to maintain their standard of living, or even leave a legacy to your favorite charity. A life insurance policy should ease your mind, because you’ll know that your loved ones will be free of any financial burdens.

Why Life Insurance is Important for Physicians

As a physician, you have dedicated your life to taking care of others. Life insurance exists to take care of your family and loved ones when you’re longer here. It gives them financial peace of mind and helps them meet their expenses and continue their standard of living with as little disruption as possible. What that looks like is unique to each individual, but may include paying off a mortgage or business loan, covering childcare costs, or supplementing children’s education.

Your life insurance can be used to resolve any outstanding debts and unpaid bills, including some types of student loans that do not expire when you die. It also can be used to pay for funeral expenses.

If you don’t have dependents, you can use life insurance to leave a gift to a loved one or a favorite charity. And depending on the size of your estate, there may be tax benefits associated with having certain types of life insurance policies.

Scott Ravitz | President of PearsonRavitz + Insurance Expert

What are the Different Types of Life Insurance?

Life insurance comes in two main types: term life insurance and permanent life insurance.

Term life insurance is the most common and least expensive form of life insurance, with varying costs depending on age, gender, and health classification. Term coverage can span from 1 to 40 years, and the premium structure can change or remain level for the period selected. If the insured dies within the term period and the policy is in effect, the proceeds from the death benefit of the insured are excluded from the gross income of the beneficiary. If the insured dies after the term period,and no premium is paid, no benefit is paid.

TERM LIFE INSURANCE

![]() Protects beneficiaries for a specific amount of time. Can be either a limited number of years (10, 15, 20, 25, 40), or a maximum age such as 80.

Protects beneficiaries for a specific amount of time. Can be either a limited number of years (10, 15, 20, 25, 40), or a maximum age such as 80.

![]() Generally lower premiums, but provides no cash value.

Generally lower premiums, but provides no cash value.

![]() Can offer protection and help for specific expenses like a mortgage or a child’s higher education.

Can offer protection and help for specific expenses like a mortgage or a child’s higher education.

![]() Simple and straightforward coverage.

Simple and straightforward coverage.

![]() Expires at the end of the term, but you may have renewable options.

Expires at the end of the term, but you may have renewable options.

PERMANENT LIFE INSURANCE

![]() Provides lifetime protection, usually effective up to age 120.

Provides lifetime protection, usually effective up to age 120.

![]() Generally higher premiums, and has cash value that increases over time.

Generally higher premiums, and has cash value that increases over time.

![]() Cash value of the policy is available to be accessed for any reason, and can provide income after retirement.

Cash value of the policy is available to be accessed for any reason, and can provide income after retirement.

![]() Complex coverage due to various components.

Complex coverage due to various components.

![]() Coverage is permanent and terminating or surrendering a policy can be costly.

Coverage is permanent and terminating or surrendering a policy can be costly.

Unlike term life insurance, permanent life insurance does not expire after a certain point as long as you continue making your premium payments. Permanent life can have a savings component and comes in several types:

- Whole life insurance has a guaranteed death benefit, regardless of when the insured person passes. Whole life also has a savings component, or “cash value,” that can grow and serve as a source of equity from which you can withdraw or borrow money as needed.

- Universal life insurance offers flexibility to adjust the premium and death benefits based on your budget and needs. Like whole life, universal life insurance offers a savings element and a death benefit, but it features different premium structures and earnings based on performance.

- Variable universal life insurance policies are considered securities contracts because there is investment risk. These policies are tied to market performance.

- Indexed universal life insurance is a type of permanent life insurance policy. It offers a cash value component and a death benefit. The policy allows for cash value growth through an equity indexed account, unlike other universal policies that only grow cash value through non-equity indexed (guaranteed interest) accounts.

Many employers offer group life insurance policies, but these policies typically are inferior to private life insurance policies for several reasons:

- They don’t offer the same control, portability or flexibility

- They’re owned by your employer

- You may only be allowed to convert the policy to the product suite that the carrier offers – which is typically limited

Some term life insurance policies contain provisions that give you the option to convert the policy into permanent without the need for additional medical underwriting. Talk to a knowledgeable broker to see if this would be a good fit for you.

Scott Ravitz | President of PearsonRavitz + Insurance Expert

What is the Cost of Term Life Insurance for Physicians?

The cost of term life insurance can vary significantly depending on several factors, including your age, health status, coverage amount, term length, and the insurance company you choose. Generally, term life insurance tends to be more affordable compared to permanent life insurance.

How Much Term Life Insurance Do Physicians Need?

There is no single answer to how much life insurance a physician might need. Instead, your coverage depends on many factors, including age, health, lifestyle, and dependents. If you’re fresh out of medical school or residency, you might be married with children, have a mortgage, and have a net worth of zero or less. While most student loans (check with your lender) disappear when you die, a mortgage could continue.

Other considerations include children’s needs. Will your children need additional funds for education? What about your spouse? Will insurance cover you if something happens to them? If you’ve got a mortgage, chances are you have other debts. How will your insurance accommodate your family?

What Should Doctors Expect when Applying for Term Life Insurance?

Applying for term life insurance typically involves filling out detailed medical paperwork and potentially undergoing a medical exam. Carriers will inquire about your family medical history, occupation risks associated with being a doctor, and lifestyle habits such as smoking or recreational activities. The good news is that once you have your policy placed, you can enjoy the peace of mind knowing that your loved ones will be financially protected.

Who are the Carriers for Life Insurance?

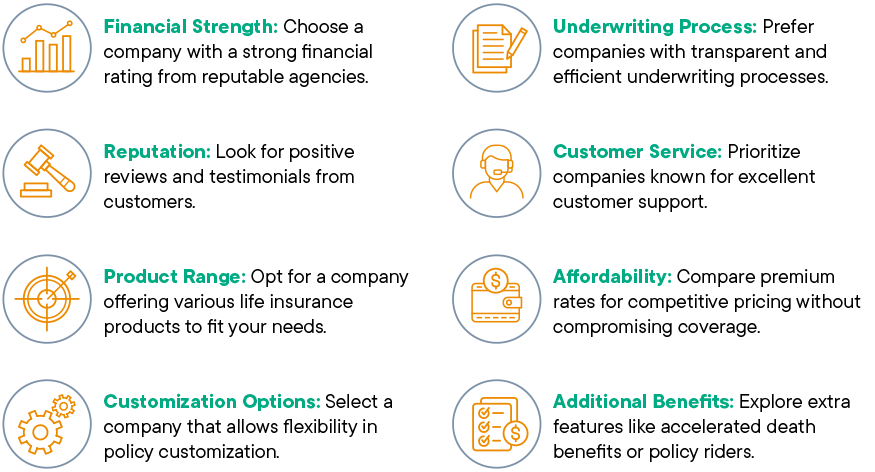

There are numerous insurance carriers that offer life insurance policies to individuals and families. Because there are so many carriers that offer life insurance policies, it is important to ensure that the company you work with is reputable.

When evaluating life insurance companies, consider these key factors:

At PearsonRavitz, we only work with life insurance carriers who carry an A/A+ rating in these areas. While these carriers can often be slightly more expensive than their lesser rated counterparts, we recommend only purchasing policies from highly reputable carriers to ensure that you have protection you can count on when you need it the most.

Scott Ravitz | President of PearsonRavitz + Insurance Expert

When Should I Get Life Insurance?

There is no better time than now — when you least expect to need it — to purchase life insurance.

We also suggest revisiting your policy when you have an important life event:

(*Women should get coverage prior to first pregnancy, as gestational diabetes and other abnormal outcomes of pregnancy can greatly increase the cost of coverage)

FAQs for Physicians Considering Life Insurance

What is life insurance and why is it important for physicians?

Life insurance provides financial protection for your loved ones in the event of your death. As a physician, it ensures that your family can maintain their standard of living and meet financial obligations if you’re no longer here. It covers expenses like mortgages, business loans, childcare costs, and funeral expenses.

What are the different types of life insurance?

Life insurance comes in two main types:term life insurance and permanent life insurance. Term life insurance offers coverage for a specific term, while permanent life insurance provides coverage for life and includes options like whole life, universal life, variable universal life, and indexed universal life.

How much term life insurance do physicians need?

The amount of life insurance you need depends on factors like your age, health, lifestyle, financial obligations, and dependents. Consider your mortgage, debts, children’s age and education, and spouse’s financial needs when determining coverage.

What should doctors expect when applying for term life insurance?

Applying for term life insurance involves filling out detailed medical paperwork and possibly undergoing a medical exam. Carriers will inquire about your family medical history, occupation risks, and lifestyle habits. Once your policy is in place, you can enjoy peace of mind knowing your loved ones are financially protected.

Who are the carriers for life insurance?

Many reputable insurance carriers offer life insurance policies. It’s essential to choose a company with strong financial ratings, positive customer reviews, and a variety of product options. PearsonRavitz partners only with carriers that maintain high ratings and offer reliable coverage.

When should I get life insurance?

It’s never too early to purchase life insurance, especially during residency when premiums are lower. Life events like marriage, parenthood, or buying a home are also ideal times to revisit your coverage needs.Women should get their first policy in place prior to their first pregnancy. Gestational diabetes and other abnormal outcomes of pregnancy can greatly increase the cost of coverage.